Imagine you met a nice couple, in every respect normal, upstanding citizens, but then learned they had retired completely from work in their early 40s. That’s right, as their kids were concentrating on college, these parents were focused on life without ever punching a timeclock again.

While that’s unusual in our world today, it’s not impossible. You may even know a few overachieving folks who have done it.

But that’s not all that is unusual about this couple. What if you also found out that they paid exactly zero in income taxes on the money they pulled out of their investment portfolios to live on?

That might sound a little fishy, right? …but, there’s even more.

What if you then learned that they never paid any tax on their earnings while they were working, and they have paid exactly zero taxes on their investment gains over the years as well. Essentially, this couple never paid taxes … EVER.

Curious now? Think maybe something illegal is going on? Wondering if they’ve changed their identities to hide from the IRS? Actually, that exact scenario is, believe it or not, both 100% possible and completely legal.

Certain Death and Taxes

In this world, nothing can be said to be certain, except death and taxes. –Benjamin Franklin

Everybody hates paying taxes, and every political season we have endless debates about how to revise the tax code so that everyone pays their “fair share.” But the truth is that the tax code is an evolving maze of rules that cannot even remotely be called anything close to “fair.” Once you start digging into it, you find some pretty darn weird things.

actually Dwight, there’s a better way…

And so, knowing the considerable opportunities to reduce taxes for those patient (or masochistic?) enough to wade through those rules, I got to wondering the other day if it was possible, at least in theory, to micro-manage your income and deductions so perfectly every year, that you never actually paid ANY Federal income taxes, and yet still were able to make a decent living and even retire early?

Sounds impossible, right? If you make a decent living, you’re generally paying taxes and lots of them. While that is normally true, here are some facts you might not know about our tax system…

- The tax code is what they call “progressive,” meaning your actual tax bill goes up tremendously with each additional dollar of income you earn. (Check out this chart to see how progressive it is, and this analysis to see how it used to be even more so).

- While everyone pays “payroll taxes” (or “self-employment taxes” for non-employees), almost half the population does not actually pay any Federal income taxes each year.

- Instead of paying taxes, many people actually get paid by the IRS instead. This happens through refundable tax credits (such as the Earned Income Credit and Child Tax Credit).

These are just a few examples of many. So given the oddities of our tax code, I began to think this might be possible. After all, I’ve seen tax returns for millionaires that showed zero in taxes before…

The Challenge

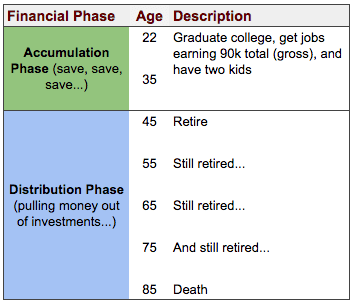

Before we go on, let me clarify the challenge set before us. As I mentioned above, this is a hypothetical test-case of whether it is possible, at least in theory, to go a whole working lifetime, retire early, and never pay taxes. More specifically, here is the basic life outline of our test-case couple …

Now clearly, for them to retire early, they are going to need to earn solid investment returns on their retirement savings. (Read more about what kinds of investment returns you can expect in the market.) And remember, we are going to try to avoid paying taxes on all of these investment gains, even though the power of compounding interest means there will be millions in gains by the end of life.

And then, for the most challenging part of all, we have to eliminate all taxes and penalties when we withdraw that money, which is difficult because our test-case couple will need to access their funds way before they’re “supposed to” in retirement.

You’ve probably heard about the 10% early withdrawal penalties, right? Generally, they apply when you take money from tax-deferred retirement accounts before age 59 1/2. So, we will need to avoid those while pulling thousands of dollars out each month to live off of in our 40s and 50s.

Clearly, the task before us is not just like beating Uncle Sam at a friendly game of cards. We’re talking about full-on, Oceans Eleven-style, walking into his own house and taking him for all he’s worth.

A Good Spreadsheet is Man’s Best Friend

When this idea first popped into my head, I knew that it might be possible to lower taxes significantly, but I was actually very skeptical that they could be lowered all the way to zero, especially for someone with a moderately high income. So, I did what any money nerd would do, I built a spreadsheet.

But before I dive in (don’t worry, I’ll spare you all the gory details), let me make a couple of caveats:

- First, if you want to see the spreadsheet, just email me. I’ll be happy to share it with you (via Google docs).

- Second, this isn’t a “fancy” financial strategy involving whole life insurance, real estate 1031 exchanges, or corporate tax schemes. (I’ll write more on why these typically don’t work later…)

- Third, the biggest caveat is this strategy simply requires aggressive retirement savings, as you will see. But that is true of any would-be early retiree … (Internet moguls, professional athletes, and pop stars excluded.)

Accumulation Phase: Save for Retirement Tax-Free

In the spreadsheet, I modeled the lifetime of a “normal” couple of college grads. I assume both of them worked and earned a combined total income of about $90,000/year. (That income can be broken down between the two of them in a variety of ways, as long as they both work and contribute to their 401ks.)

These two college lovebirds are married and therefore file a joint tax return. They have also been blessed with two darling kids. (The kids and married status help to lower taxes significantly, so this would admittedly be much harder, if not impossible, for a single person. That’s not to say many single people couldn’t use the same strategies to greatly reduce their taxes, however.)

Now, being driven and disciplined savers, they decide to max out their 401ks at work from day one. In 2017, the 401k limit per person is $18,000, so they saved $36,000 total in their workplace retirement plans.

In addition, they also both contribute to a Roth IRA, which allows up to $5,500 per person, for a grand total of $47,000 of savings, or 52% of their gross income.

That sounds like a lot, because it is.

(thanks, Captain Obvious)

But stick with me, because while I get that this is an extreme example of living for tomorrow, I think the tips you can draw from this can be very useful, even for those pursuing a little more of a “balanced” lifestyle. (And if you’re reading this and thinking, “geez, I can’t even get out of debt, this doesn’t apply to me,” take a look at how I paid of $40k of debt for some helpful tips on that.)

By contributing to their 401ks, our couple is deferring their income into the future. From the IRS’s viewpoint, they did not receive that income this year, and so they don’t have to pay income tax on it this year. In other words, they have deferred that income until they decide later on down the road to take the money out of the 401k account.

Maxing out their 401ks is a very important part of why their tax bill goes all the way to zero. Why? Because their taxable income is lowered to a point where the magic of tax credits kicks in.

How Tax Credits Work for You

Tax credits are one of those weird “quirks” in the tax code, and they are a wonderful thing for those who qualify.

That’s because tax credits are much more valuable than tax deductions, because they are a dollar for dollar reduction in taxes, whereas a tax deduction only lowers your tax bill by your marginal tax bracket.

And example might help.

Let’s say you are someone in the lowest tax bracket (10%). If you have tax deductions, then for every $1 of deductions you claim, the IRS will lower your taxes by 10% (your tax bracket). However, a tax credit will always reduce your taxes on a dollar for dollar basis. In other words, $1 of tax credits will reduce your tax bill by $1.

Therefore, in this case, a tax credit is actually 10x more valuable than a tax deduction. Why? Simply because a $1 tax deduction reduces taxes by 10 cents, whereas a $1 credit reduces your taxes by $1.

What’s more, tax credits can even make the IRS pay you even if you don’t owe any taxes at all! These are called refundable credits, and two of the best refundable credits are the earned income tax credit and the child tax credit. Both of these credits are limited by income, so by funding their 401ks, our couple has lowered their income sufficiently to qualify for these and other credits.

Still, you may be wondering how this couple survived if they put all that money into retirement accounts. They do, after all, have two kids who like to do annoying things like eat on a regular basis.

Well, I had the same question, so I ran the numbers and came up with a monthly budget of about $3,500/month, including the refundable tax credits. They still have to pay the mortgage, utilities, food and all the other costs of daily life on that amount, so they aren’t “living large” by any means. Still, it’s possible, at least in theory.

How to Pay Zero in Taxes: The Numbers

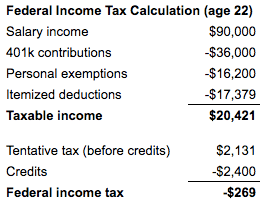

So here are the numbers for that first tax-year, so you can put it all together:

Having four members of their household means they get four personal exemptions, at $4,050 each, and I’ve assumed that they have the average number of itemized deductions in the U.S., per a recent CCH tax study. These two deductions, when combined with their 401k contributions, get their taxable income down to about $20k. That’s enough to get them very close to the lowest Federal tax bracket, so the vast majority of that remaining $20k is taxed at just 10%. However, once you factor in the tax credits, it drops to zero (and they even get a small refund.)

Distribution Phase: Retire Early and Withdraw Funds Tax-Free

So far, so good. We’ve seen that, at least for our fictitious couple, it is possible to pay zero taxes while working and saving for retirement. And since they are saving so aggressively, it’s probably not hard to believe that they’ll be able to retire very early, assuming a decent investment return.

However, believe it or not, that was the easy part.

The problem is that all that money sitting in their 401k has never been taxed, remember? And the IRS is salivating over that money like a puppy at the dinner table. Normally, all of those dollars would be taxable when they are withdrawn, but we’ve got a trick up our sleeve…

Before I get there, however, I need to briefly recap the rules. While the 401k contributions are pre-tax, the money in their Roth IRA accounts is considered “after-tax” money. This is because the contributions are made after your income is already taxed in the year you made it. However, the money in the Roth IRAs can grow and generally be withdrawn tax-free in retirement. (For more on whether you should contribute to an IRA or a Roth IRA, read this.)

So assuming a simple 8% compound growth rate on their investments, our frugal couple can retire in their mid-forties, just over 20 years into their working lives.

At their retirement they would have several million dollars in their portfolio, 75% of which would be sitting in the 401ks and the rest in the Roth IRAs. (The 401k funds would probably be rolled into a Traditional IRA at this point, but the tax ramifications are the same.)

Now remember, our couple is only in their mid-forties, still about 15 years younger than the IRS-approved retirement age, which means getting money out of retirement accounts normally faces a 10% penalty in addition to any regular taxes due.

This is where establishing and funding their Roth IRAs early in life is vital. You see, the Roth IRA has a 5-year window on contributions AND conversions that must be met before withdrawals can be made tax free.

So, the beauty of this plan is that they established their Roth IRA years earlier, so they don’t need to worry about the 5-year window on their contributions. And, since they have been funding the Roth IRAs at a high level for a long time, they have a lot of principal built up in the Roth accounts. That means they can rely on tax-free withdrawals of their principal in the first five years of retirement, which is crucial because if they had to touch their earnings, it would be taxed since they are not yet 59 1/2.

Meanwhile, during the first five years of retirement they can also make Roth conversions (transferring money from the 401k/IRA to the Roth), so that at the end of the five years, they can pull money from the conversions portion of the Roth IRA account, instead of earnings.

The trick in this whole strategy lies in the order in which withdrawals from Roth IRAs are made. Per IRS rules, any withdrawal from a Roth IRA is taken first from the original contributions (or your principal). Once all the contributions have been withdrawn, the IRS deems any withdrawals to come from conversion money next, and then earnings last.

What’s This About Roth IRA Conversions?

A Roth IRA conversion is simply when you take money from a Traditional IRA and move it (“convert” it) to a Roth IRA. Because Traditional IRA dollars are pre-tax, you must pay taxes on money that you convert to a Roth IRA.

So while our couple are living off of the tax-free withdrawals of principal from the Roth IRA, they are simultaneously converting money from the IRA to the Roth IRA to replenish it as they go. That process kickstarts the 5-year window on the Roth conversions at retirement and allows them to be able to use that money tax free as soon as the 5-year window is completed.

You may be asking, but wait, if they do Roth conversions, won’t that cause them to have taxable income? Yes, normally it would. However, they will convert only the maximum dollar amount allowable to bring their tax bill to exactly zero. In other words, they will convert just enough to take advantage of the personal exemptions, itemized deductions, and tax credits, but not bring the actual tax bill above zero.

So, with this process, they will begin filling the Roth IRA conversion “bucket” even while they are draining (living off of) the Roth IRA contribution (or principal) “bucket.”

And that’s it! We just rinse and repeat this process going forward, converting money from the 401k/IRA bucket to the Roth IRA, while simultaneously pulling money for living expenses from the Roth IRA itself.

Key Takeaways

While this case study presents a picture of extreme frugality just for the sake of paying no taxes and retiring early, that doesn’t mean we can’t learn from it. For me, just crunching the numbers was hugely helpful to think through the mechanics of how the tax code actually works in practice.

And I hope this was more than just a fun mental exercise for you as well. In fact, I think it’s clear that there are several helpful tax tips almost anyone can profit from. Here are several that jump out at me:

- Contribute as much as you can to 401ks. I occasionally talk to people who “don’t believe” in 401ks, and that’s just crazy. Not only do you get a tax deduction and possibly matching from your employer, but also you may be able lower your taxable income far enough to qualify for tax credits and other unusual, income-based incentives.

- Start a Roth IRA as early as possible. The only way this couple could pull money out of their Roth IRA at retirement without penalty is they had started the account at least five years beforehand.

- Contribute as much to the Roth IRA as possible, if eligible. You can pull contributions out of a Roth IRA at any time, without penalty and taxes, as long as you’ve met the 5-year window. Therefore, the more you contribute early on, the more flexibility you will have to use those funds later in life if you need to.

- If not eligible for a Roth IRA, consider a “Backdoor Roth IRA.” There is a way to contribute to a Roth IRA even if you make too much income.

So, what do you think of this crazy strategy? Questions or comments? Leave them in the section below…

{kind=link}