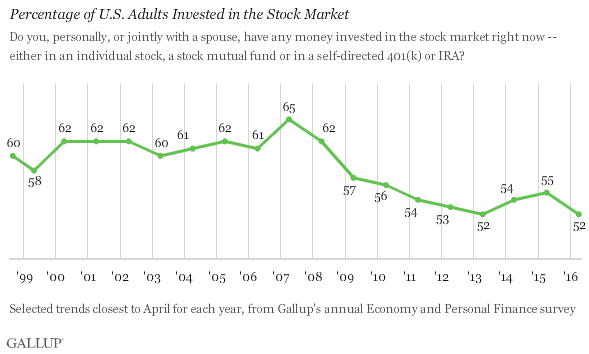

Here we are in 2016, eight years into a strong stock market rally with a total return on the S&P 500 of over 200%, and yet I’m always amazed to talk to people who are still sitting in cash on the sidelines. I mean, on the one hand, I get it. Lots of folks are more focused on paying down debt or just generally mistrustful of the market in the aftermath of the recession. But either way, more and more people seem to be skeptical of the wisdom behind holding stocks as a long-term wealth building tool. In fact, a recent Gallup poll shows that the percentage of U.S. adults who are invested in the stock market are at a record low.

Millennials, who are mostly too young to remember the really good markets of the 80s and 90s, are especially distrustful. In fact, a recent Goldman Sachs survey found that only 18 percent of young american adults trust the stock market as “the best way to save for the future.”

But what they don’t know is that saving for retirement can be, in a way, remarkably easy. Especially for those with time on their side. The numbers aren’t really that hard. I won’t detail them all here, but suffice it to say that “simply” saving 10% of your income for retirement each year from age 25 to 65, provided you achieve somewhere close to historic stock market rates of return, is all you need for a comfortable retirement.1 While this may not be easy, it’s certainly a possible goal for most people to strive for.

On the other hand, if you plan to simply save enough in cash to retire, without investing, things get quite a bit more difficult. Using those same assumptions as before, the average American household would have to save about 60% of their income, assuming their investments only keep up with inflation.

That’s sixty percent of your gross income. Six – zero. And that’s before any taxes are taken out. After taxes, that’s almost everything. Forget rice and beans… more like living on cheerios and water.

So, what do I tell someone, especially a young person, who thinks investing in stocks is just too “risky?”

Everything in Life Involves Risk

The truth is that everything in life involves risk. Which is just another way of saying that we don’t know the future. Maybe North Korea sends us all into the dark ages with a rogue nuclear attack. Maybe a highly mutant strain of the black plague reappears. Maybe the world economy collapses and sends us all back to the barter system. These are technically all possible. It’s also possible that I accidentally walk out in front of a car after finishing this post.

We aren’t promised tomorrow.

I say this just to put the concept of risk into context. At the end of the day, all investing involves some form of risk, and while there are ways to reduce risk, it’s impossible to completely eliminate risk from investing. This is, again, simply because we don’t know the future.

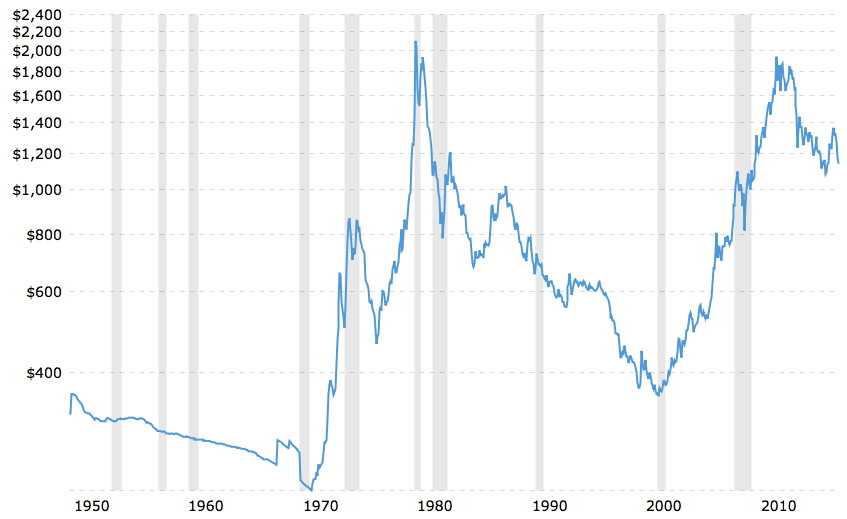

Think putting all your savings into cash is “risk-free?” What if we have hyper-inflation? In that scenario your cash is losing value just like stocks and bonds can. Well, then what about gold? Sadly, you have the exact same problem there, as the following graph shows. Prices can be extremely volatile both on the up and downsides, and surprisingly, gold does not always offer a good hedge against bear markets (recessionary periods shown in grey).

Gold Prices since 1950 (inflation-adjusted) | source: macrotrends.net

What is Risk?

But when we talk about risk, it’s important to define our terms. The most important definition of risk is a permanent loss of capital. This can happen when you make bets on a single company’s stock or when leverage (i.e. debt) is used improperly. A single company can go bankrupt or lose most of it’s value almost overnight, and for reasons that are sometimes practically impossible to foresee (e.g. Countrywide, Enron, Bear Sterns, etc.) But for a very diversified portfolio of stocks like the S&P 500, some very deep and radical damage to our economic system would have to occur to permanently destroy all of the value of those underlying companies.

But usually when the average person talks about risk in the context of the stock market, they’re not so much referring to the end-of-the-world scenarios as they are a general unease with the volatility inherent in the market. In other words, it just feels unsafe that the value of my nest egg can drop down so quickly, and sometimes even violently. Worse, the changing values blinking at us from our computer screen seem to be controlled by forces entirely out of our control — by terrorist attacks, or central banks, or geopolitical instability in far-flung places.

So for my purposes here I just want to focus on risk in the form of volatility in the markets. Is volatility something to be worried about? Again, perspective is critical for thinking carefully about this topic, so for comparison let’s take a look at something almost everyone is comfortable investing in: a personal residence. In America, it’s almost a cultural religion that owning your own home is not only the “American Dream,” but also one of the smartest investments one can make. And so no one bats an eye at the idea of sinking thousands of dollars into your house, even though for most people it is by far the largest investment they make and probably not a very good one. It’s just generally understood that real estate is more “stable” than stocks. While stocks go up and down on a daily basis, real estate does not.

As An Investment, Your Home Faces Risks Too

Now I realize that for most people, your home isn’t just an investment. It’s also a lifestyle decision, a place to build a home and become part of a community, and much more. But let’s look at it from strictly an investment perspective for a moment. Or better yet, let’s look at a current day, real-life example of real estate in an investment context.

In the city of Miami there’s a trendy, upcoming neighborhood called Wynwood that has experienced quite a renaissance of life, character, and economic activity. Originally a working-class Puerto Rican settlement known as “El Barrio,” the area is now known as much for its gentrification and high-priced neighborhoods as it is for world-renown works of graffiti and uber-hipster cafes. And for property owners in Wynwood, the last few years have been kind. According to real estate website Zillow, the average home price is up 187% since 2010. If you compare that with a 126% increase for the overall US home price market (based on the Case-Shiller index), you can see that the neighborhood has been flying high for a while.

However, all of this is before the news of the Zika virus’ arrival. As you can imagine, the fear accompanying this heretofore unknown disease was not positive for local real estate prices. In fact, reports have already begun to trickle out that businesses are beginning to close, tourism is starting to wane, and residents are staying indoors. If it turns out to be a serious, long-term threat to residents’ quality of life, the once booming area of Wynwood may suddenly have plenty of supply but very little demand. Economics 101 tells us that in that scenario, there is only one direction for housing prices to go.

(Update: since this post was originally written, the Zika virus has been more or less contained; however, it could have easily been worse. Either way, this is just a thought experiment to make a broader point, and I wish the people of South Florida a swift recovery from this terrible disease.)

Now let’s think about this example for a second: here is a threat that came pretty much out of nowhere. Certainly, very few (if any) recent homebuyers factored the threat of a heretofore undiscovered virus touching down on our shores into their analysis of the home they wanted to buy. My point is there are many risks out there that can affect all investment assets, including houses, and there are some risks that are impossible to plan for or attempt to mitigate.

How Stocks and Real Estate Are Different

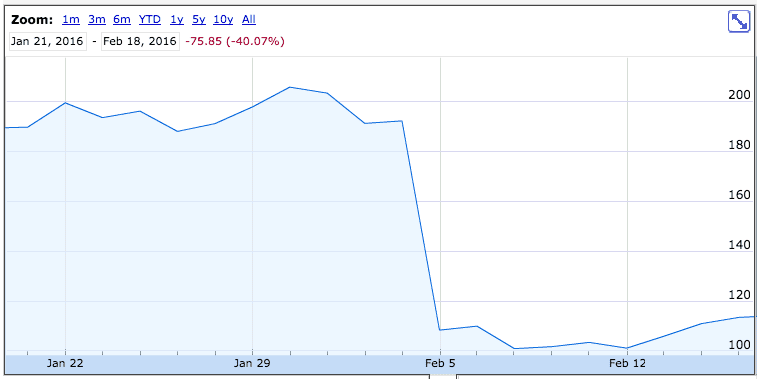

One key difference between the stock market and real estate is that in the stock market, new information is almost instantly reflected in asset prices. For example, when LinkedIn missed expectations on their quarterly earnings call, the stock immediately plummeted (see chart below). As an investor, there was no way to see that coming, neither the company’s performance nor the market’s reaction. (Unless you had insider information, of course, but that’s illegal to act upon.) However, in real estate, you only know the true price if you put the property up for sale. So just because you don’t see the ups and downs on a daily basis, doesn’t necessarily mean that the value isn’t changing.

source: Google finance

What If Your House Was Traded Like a Stock?

Consider this scenario as an example: one of your neighbors is extremely interested in buying your house. So interested, in fact, that every day he comes by the house, rings the doorbell, and has a firm offer for you to consider — take it or leave it. He has a contract in hand, and all you have to do is sign it and the deal is done. Do you think he would offer you the same amount every day? Or would he offer more on some days, and less on others? Maybe over a period of time his offers would vary, and on some days, he raises his price a little to tempt you to sell. These might be days perhaps when he’s in a slightly better mood, when he just got a raise at work, or when he is getting along better with his wife.

Other days he might offer a slightly lower price, but either way, let’s assume he comes by your house every day with an offer, without fail.

Now let’s introduce additional variables. Let’s say just down the street it’s announced that a brand new football stadium is to be build, and that a few blocks the other direction, a major corporation announces that it is moving its headquarters in bringing hundreds of high-paying jobs. Would this change his offer? Clearly, because of these new developments he would expect higher values in the future, so his offer might go up.

On the other hand, if your little fictional neighborhood suddenly gets hit with an earthquake or a mysterious virus, such as the Zika threat described above, that would have a drastic effect on his offer as well. He might be afraid that businesses would move out of the area, houses would sit vacant, roads would be unrepaired, etc.

Is Real Estate Really Safer?

My point with all of this is NOT to say that your house is any more or less volatile (or “risky”) than other investment classes. There’s a place for both real estate and stock investing, in one form or another, for almost everyone. (And yes, if your trained in finance, I do realize that different investment asset classes have different risk profiles historically. This post is not geared towards you, it’s for the layperson who is perennially afraid of stocks, and therefore falling behind financially over the long-term.) My point is just to say that volatility in the stocks markets, in and of itself, doesn’t indicate that stocks are risky. Volatility is just a function of the fact that the stock market is highly liquid (e.g. there are lots of buyers and sellers, and shares can be sold quickly.) With real estate, you don’t see the volatility because the property isn’t priced on a daily basis. The big take-away is this: if your personal residence sold like a stock on a market exchange somewhere, you can bet that it would also be volatile.

When Stocks Are Actually Less Risky

In some ways, I could go even further and argue that a large basket of stocks (such as a mutual fund, index fund, or ETF) can actually be LESS risky than an investment in a single real estate property, simply due to the fact that a basket of stocks is more diversified.

Returning again to the S&P 500 index fund, as an example, it holds approximately 500 large multinational companies in many different sectors of the economy. As of this writing, it has allocations to companies in the following areas:

- 20% Technology

- 15% Healthcare

- 13% Finance

- 10% Energy

- 22% Consumer Goods

- …and more.

What is the chance of all 500 companies in different sectors going bankrupt all at the same time? What is the chance that all of the various industries represented become obsolete? Now, what is the change that one real estate property loses its value. Both are pretty low probability events, but you could argue the basket of stocks is actually the safer investment of the two.

Warren Buffett, the famous investor, agrees. He writes in a recent shareholder letter,

Stock prices will always be far more volatile than cash-equivalent holdings. Over the long term, however, [cash] instruments are riskier investments – far riskier investments – than widely-diversified stock portfolios that are bought over time. …. Volatility is farfrom synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.

It is true, of course, that owning equities for a day or a week or a year is far riskier (in both nominal and purchasing-power terms) than leaving funds in cash-equivalents. That is relevant to certain investors…

For the great majority of investors, however, who can – and should – invest with a multi-decade horizon, quotational declines are unimportant. Their focus should remain fixed on attaining significant gains in purchasing power over their investing lifetime. For them, a diversified equity portfolio, bought over time, will prove far less risky.

Conclusion: Don’t be Afraid of Stocks If Held for the Long-Term

Don’t believe the myth that stocks are too risky to invest in. As long as you understand your risk tolerance, have a long enough time horizon, and stay diversified, stocks can be a valuable wealth building tool. In modern America, in fact, with 401ks, IRAs, and Roth IRAs at our fingertips, almost all of us will need to invest in stocks over the course of our lives if we want to retire, and just because they go up and down over the short term doesn’t mean a patient investor won’t make significant money over the long term.

1This assumes the following: an investor with the median U.S. household income (currently about $50k/year), a saving rate 10%, an investment return of 11% on average (the average annual return of large and small US company stocks since 1926 is about 10-12%), and a 3% inflation rate. At age 65, this hypothetical investment portfolio can withdraw 4% (which most academic research has shown to be a safe withdrawal rate) and replace the inflation-adjusted pre-retirement income. Social Security retirement benefits are not included.

{kind=link}