The Acorns investing app is a unique combination of automated savings and automated investing. I’ve written before about why I believe automating your investments is vital to long-term investment success, and also why “paying yourself first” is an easy way to make sure you save for long-term goals such as retirement. Acorns is an innovative way to accomplish both goals together, as it automates both the saving and investing processes together in one platform. Overall, the Acorns investing app has a lot of good features, but it’s not a replacement for your main retirement savings plan, simply because Acorns doesn’t offer tax-deferred retirement accounts at all. For that reason, it’s best used for more intermediate-term goals, such as saving for a new car or house downpayment.

My Re-Introduction to the Acorns Investing App

The other day I walked down to the sports bar down to watch a game and grab a beer. I was there alone on this occasion, so I got to chatting with the people around me about the game and a few other things. The guy sitting next to me asked me what I did for a living, and we inevitably got to talking about money and investing. Of course, that’s always a fun conversation to me, so we enjoyed batting around various investment strategies while the game went on in the background.

Then he asked what I thought of the Acorns app. I told him I had heard of it, but that it wasn’t something I had personally used. Walter, whose name I learned later, then told me that he had signed up just a few years ago, and had put in only $500 of seed money at the beginning. Amazingly, now his account is worth over $20,000!

(Of course, a few of my skeptical alarm bells are going off in my head at this point, but more on that in a minute.)

What is Acorns?

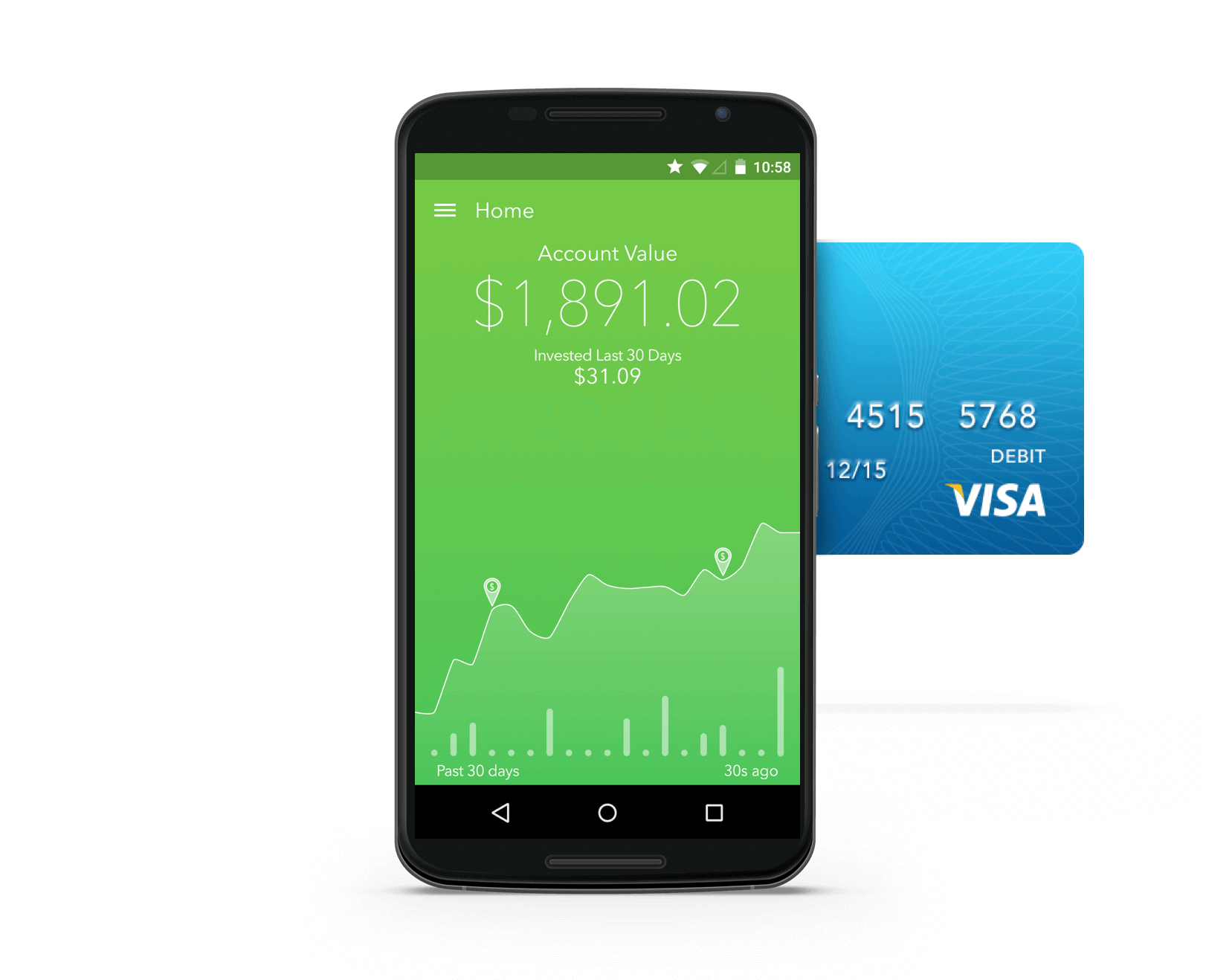

First, I should back up and describe what Acorns is. It’s simply an app that tracks your purchases (on credit or debit cards), and rounds each purchase up to the nearest dollar. Then the extra “change” is invested for you in an investment account.

How this happens is that you link your credit and debit cards to the app on your smartphone, and it tracks your purchases as you make them. It has a slick interface where you can see the money you’ve invested and track your portfolio. All the investment management work is done for you on the back-end, so you can sit back and watch your money grow. And trust me, as someone who has made thousands of tedious, manually-entered trades in my life, that’s a really nice perk.

So that’s the basic idea, but what I like the most about Acorns is that it simply automates the process of saving money. If you’re anything like me, making an active decision to save money is hard, so I usually procrastinate and never get around to it.

But, if it happens automatically, I’ll save a heck of a lot more. Overall, this is a win-win: you save money, Acorns helps you invest it, and the whole process takes about 10 minutes or less to set up. It’s that easy and simple.

What Kinds of Investments Does Acorns Provide?

The Acorns app takes the guesswork out of investing by providing diversified, low-fee portfolios for various risk levels. You can choose between conservative portfolios all the way up to high-octane, aggressive asset allocations. The design of these portfolios is based on Nobel-prize winning methodology known as modern portfolio theory. While I don’t believe that MPT is the final word on asset allocation (I prefer a more tactical approach), this is a great place to start for most people. It’s a much better idea than trying to trade stocks or trying to pick stocks yourself, at least for most people. (If you’re interested, check out why you shouldn’t waste your time picking stocks here.)

As you probably know, generally speaking, the more stocks you have in a portfolio, the more aggressive it is. That’s because over time stocks generally provide the best investment returns compared to other asset classes, but they also can go down in value tremendously when times are bad. (For more on what kinds of returns you can expect from stocks, check out this recent post.)

You can add real estate stocks to that category as well because although they are based on actual real estate, the investment itself is traded as a stock on the stock market. (Any real estate investment inside a mutual fund or ETF “wrapper” is typically held in the form of a REIT, which is traded like a stock on the stock exchanges. Without going into a lot of detail, REITs generally have similar risk and return characteristics as stocks, meaning they can go up a lot in the good times, but also post large losses in the bad.)

The broad breakdown of Acorns’ portfolios are as follows (as of today):

| Portfolio | Stocks (and Real Estate) | Bonds | Expected Long-term Return* | Expected Average Bear Market Loss* |

| Conservative | 40% | 60% | 3-6% | -5 to -10% |

| Moderately Cons. | 51% | 49% | 4-7% | -10 to -15% |

| Moderate | 61% | 39% | 5-8% | -15 to -20% |

| Mod. Aggressive | 74% | 26% | 6-10% | -20 to -25% |

| Aggressive | 89% | 11% | 7-12% | -20 to -30% |

Again, I would refer you to my post about the long-term returns of stocks, but these broad stock/bond breakdowns are the key driver of returns for your Acorns account, and the more aggressive you the portfolio is, the more likely you are to achieve high returns over the long-term.

What About Fees?

Aside from the automated savings feature, Acorns is, at its heart, an automated investing platform. That means it is competing with other “robo-advisors” such as Betterment, Schwab Intelligent Portfolios, and Wealthfront. So you would expect its costs to be low, and they are.

They charge $1/month until you’ve saved $5,000. After that point, they are simply 0.25%/year. (In addition, for college students with a .edu email address, they will waive all fees for up to four years.)

This cost structure puts them right about the same as the other platforms, with both Betterment and Wealthfront at 0.25%/year as well, but Wealthfront waives the fee for the first $15,000 invested. Schwab Intelligent Portfolios is actually free, but with the caveat that they have a larger cash position than perhaps most investors would like, which serves to compensate Schwab through money market management fees.

The bottom line is that Acorns is very competitive from a cost perspective. However, my recommendation would be to “seed” your account with $5,000 up front to qualify for the 0.25% price structure. While $1/month doesn’t sound like much, it’s actually almost 2.5% on a small balance of $500. That kind of fee structure can really eat into your returns over time.

How Did Walter Go from $500 to $20K in Three Years?

Okay, let’s get back to Walter.

Initially, I was skeptical of his claim that he had started with just $500 a few years ago and ended up with $20K today. But obviously, not all of that is investment gain. Some of it is just his own principal from purchases that were rounded up. On top of those investments, Walter told me he set up a monthly deposit into the Acorns investment account of several hundred dollars (I don’t remember the exact amount.) That is very simple to do once you have your bank accounts linked to the Acorns app… just a few clicks and you are done.

So, even if none of the $20k he saved is from investment gain, the fact that he saved that much money over three years is pretty cool in and of itself. That would make a pretty nice down payment on a new car, or maybe a couple of fancy vacations.

But clearly, some of it is investment return, because over the last three years, despite all the hand-wringing and negativity we’ve seen in the news, stocks have done pretty well.

Here are the returns of the S&P 500 for the last 3 years:

- 2014: 13.96%

- 2015: 1.38%

- 2016: 11.96%

While I don’t have enough data to figure out exactly what his returns were, but the bigger point is that you can save a decent amount of money without even trying or realizing it by using the Acorns app. Once you have a nice balance saved up, compound interest begins to kick in, and the money you make begins to make money of its own.

So if you’re interested in giving Acorns a spin for yourself, check it out here.

Expected Long-Term Return: This refers to a range of average annual returns that investors in these portfolios are most likely to receive over long-term time horizons (20+ years), assuming they perform in the future generally in line with the past. (Past returns are based on data from the S&P 500 index and the U.S. government and corporate bond market returns provided by Standard and Poors.) However, I have discounted the returns slightly due to the low level of interest rates currently, and it’s important to note that these are my estimates only and not a prediction of the future. Of course, past performance is no guarantee of future results.

Expected Average Bear Market Loss: This refers to the average range of losses experienced by a portfolio similar to this during past economic recessions. Because reliable data for some asset classes (such as emerging markets) only goes back a few decades, these estimates reflect only the experience of U.S. based stock and bond markets. Of course, future recessions can (and will) look different from the past and there is no guarantee losses will not exceed these thresholds. These are provided for reference and to provide general framework for evaluating the various investment options, and are in no way a prediction of the actual future performance of these specific portfolios.

{kind=link}