What if there was just ONE thing that, if you did it, you could almost guarantee that you won’t be broke in retirement?

What if there was ONE financial decision that is an almost guaranteed “no-brainer?”

Well, there is. It’s called a Roth IRA.

There aren’t many things in personal finance like this. Sure, you can say general things like “save money,” or “live within your means,” but I’m talking about specific strategies or financial tools. Most things are good for this situation, but bad for that. Or they only work if you have A, B, and C going on already.

For the most part, the Roth IRA is not like that. It’s a financial strategy that works in the vast majority of situations, and contributing consistently to one goes a long way towards financial success.

The Roth IRA is personal finance’s version of apple pie. There’s absolutely nothing not to like.

- Tax deferred growth? Check.

- Tax free withdrawals? You got it.

- Access to pretty much any investment? Ditto.

- Access to your principal without any penalties? No problem (once you complete the 5-year test)

Of course, there are caveats. After all, this is a creation of Uncle Sam and there are always caveats. But overall, the Roth IRA is one of the best vehicles out there for long-term growth.

Now, there are plenty of places on the web that explain all the details of Roth IRAs, so I’ll just hit the highlights here. But what I hope to do differently is to relay my personal experience in using Roth IRAs, and what I’ve seen over the years with clients that have used them as well. In doing so, I hope this is a practical and useful guide to using a Roth to its fullest capacity.

First of All, What It’s Not

Now, even though I just promoted the multiple applications of Roth IRAs, in the end they can’t do everything. Here are a couple of things they are not:

Not an Investment Itself — the Roth IRA is a retirement account in which you put investments. It is not, in and of itself, an investment. It’s just an account, and the investments you put in it can be almost anything — stocks, bonds, mutual funds, ETFs, and even real estate.

Not an Education Plan — the Roth IRA does have an “exception” that allows you to withdraw funds early to pay for college expenses, but it wasn’t originally designed for this. It’s too involved to dive into the details here, but just know that while it can be useful at times to help pay college expenses, that isn’t its “highest and best use.” In most cases, other accounts are better choices for college planning.

The Power of Tax-Deferred Growth Coupled with Tax-Free Withdrawals

I’m going to assume that by now you’ve heard about the power of compound growth. The beauty of the Roth IRA, however, is that not only do you get tax deferral, you get to avoid taxes completely for any growth your money makes inside the Roth IRA.

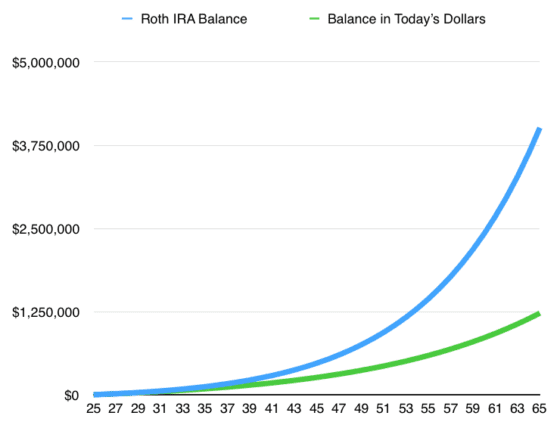

Let’s run some numbers to help this make sense. I’ll assume that Jack, who is 25 years old, employed, and starting to get serious about his finances, begins contributing the maximum amount allowable to his Roth IRA. (In 2017, that amount is $5,500). He invests it in a growth stock mutual fund, which returns on average about 10%/year. (That’s not a prediction; I’m just using the market average over the last 90 years. Let’s also assume Jack is diligent to fund his Roth IRA every year for 40 years, or until he is age 65.

Now before I talk about Jack’s retirement nest egg, there’s a couple other details we should address. First, money in the future isn’t worth as much as money today. Think about it, if I offered $100 now or $100 a year from now, which would you take? Obviously, you’d take the money now. That’s because money in the future is worth less due to inflation. Looking back over the last 90 years, inflation has run at about 3% on average. So we have to take into account that our final total needs to be adjusted for inflation, in order to talk meaningfully about a large sum of money.

The second detail is tied to the first. Because inflation is creeping along, Congress will over time increase the maximum contribution limit on the Roth IRA, and so we should assume that Jack diligently increases his contributions accordingly. For the purpose of our calculation, we will assume it goes up by 3%/year as well.

Hypothetical Example: Investing the maximum contribution, currently $5,500/year (increasing at 3%/year) in a Roth IRA that grows at 10%/year. The blue line shows the account value, while the green line shows the account value in today’s dollars.

Here’s how the numbers work. If Jack is diligent to just fund his Roth IRA each year, and he earns a decent return (again, I’m using the historic stock market return of about 10%), he ends up with just over four million dollars at age 65. More importantly, that’s about $1.25 million in today’s dollars. So, what that means is that if he withdraws a historically safe withdraw rate of about 4%, Jack can pay himself a tax-free income of $50,000 for the rest of his life.

Did I mention that’s TAX FREE INCOME!

And since that’s tax free income, it’s roughly the equivalent of $75k in salary, before taxes.

{kind=link}