I spent a year teaching high school English, and one thing I’ll never forget is the mountainous volume of papers there are to grade. I can remember many nights sitting at the kitchen table with a huge stack of papers and wondering: “how exactly did I get myself into this again?”

I also began to notice that after grading a certain number, I often became a little bit more lenient as I got to the bottom of the stack. No matter how hard I tried to grade as fairly and objectively as possible, it was just easier to give a student the benefit of the doubt as time went on, rather than make hard judgment calls. Of course, I would try to combat this problem as much as possible by taking little breaks, but eventually it would return and the cycle would repeat itself. Researchers have identified this phenomenon in the human brain and dubbed it “decision fatigue.” Apparently, just like an arm or leg muscle fatigues when we are lifting weights, our brains get tired when evaluating complex decisions.

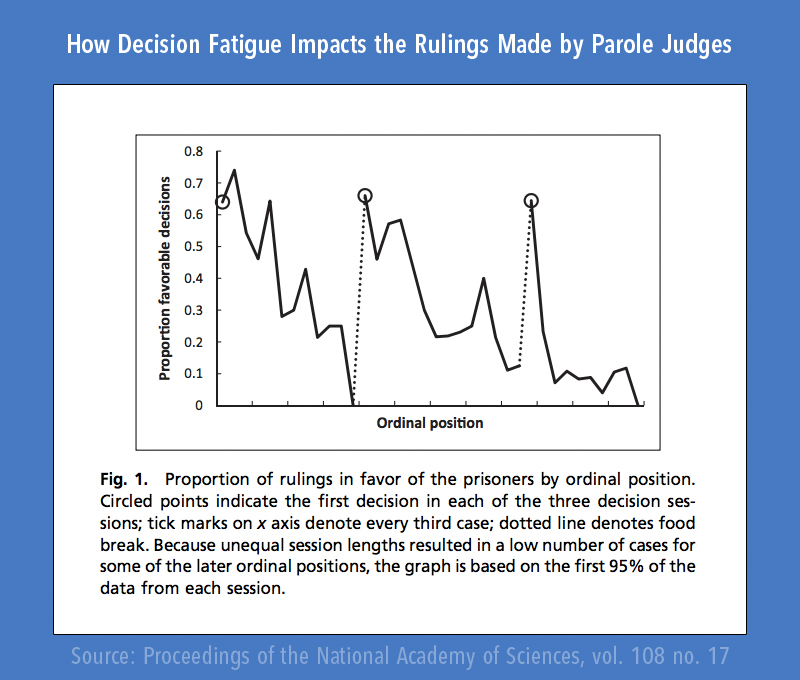

In one interesting study, researchers examined the decisions of parole judges who had to decide whether or not prisoners deserved to be set free. They found that at the beginning of the day the judges granted parole about sixty-five percent of the time, but as they began to tire, that began to drop, eventually to zero percent. In other words, lacking the mental resources to completely analyze the case, judges found it easier to simply deny parole as the day went on.

You have Only SO MANY Good Decisions Per Day

Decision fatigue affects your ability to make investment decisions as well. With all the important decisions you have to make on a daily basis, do you really have time to decide the following as well?

- Should I buy Coke or Pepsi? How about Apple, Samsung, or Google? Do I have the hours of research time available to make good decisions on this?

- Am I going to invest internationally or just domestically?

- Will I use individual stocks, mutual funds, or ETFs?

- What about small and mid-sized company stocks?

- Or bonds? Should I own them in this low-interest rate environment? If so, how much and in what vehicle? Should they be treasuries, munis, high-yield, or corporates?

These are just a small sample of the relevant questions. Sadly, decision fatigue quickly sets in for many people, leaving them with the default response of doing nothing rather than something.

Why You Should Automate Your Investments

Crucially, the most valuable resource that you have is time. Time to allow your investments to grow to the point that someday you can create an income stream that will replace your current lifestyle. That is the goal whether you just want to retire at age 65 or reach financial independence at a much younger age. But, neither goal can happen without enough time available to allow for the investment portfolio to grow.

So if you’re lucky enough to have time on your side, history tells us that saving for retirement can be, in a way, remarkably easy. The numbers are actually pretty simple: if you save just 10% of your income for retirement each year from age 25 to 65, and if you get long-term returns within the range of historic stock market rates of return, that’s pretty much all you need to do to afford a comfortable retirement.1 The key to success is the following formula:

Consistent Savings + Consistent Returns + Time = Financial Independence

On the other hand, if don’t have those three ingredients, plan to work much longer than is necessary. For example, if you don’t achieve long-term rates of return sufficiently high enough because your investment strategy is start-stop, haphazard, and often mostly in cash while you wait to decide on the perfect investment opportunities, you run the risk of falling short of your retirement goals. Very few people have enough money to afford poor investment returns, so unless you were born with a silver spoon in your mouth, you don’t have any time to waste. If the average American were to try to save enough for retirement in cash alone (i.e. without investing), things get monstrously difficult. The math tells us that the average American household would have to save about 60% of their income, assuming their investments only keep up with inflation.

Very few people save enough money to afford poor investment returns.

Trying to Time the Market Reduces Your Long-Term Chance of Success

Another reason you should automate your investment portfolio, is that the tendency to try to time the market is so strong. Last year, my brother and I set out across Europe on a vacation. This wasn’t a sitting-by-the-beach type of vacation at all; instead, we were determined to mix a once-in-a-lifetime tour across Europe with a little bit of adventure along the way. So, we scheduled a little snowboarding in the Alps, and also some time to rent a car on the german Autobahn highway system. As you probably know, the Autobahn includes some roads with no posted speed limit; it’s one of the few places on earth that you can truly experience a “need for speed.”

Now, being the practical 30-somethings that we are (well, at least sometimes), we had initially planned to rent a regular 3-series BMW for our escapades, not wanting to push it in a foreign country on unfamiliar roads. But, we were beguiled by the salesperson in the Munich rental car office to upgrade–that word, by the way, doesn’t do it justice–to a brand-new BMW M6 sportscar.

My sheepish grin in front of our rented BMW M6 next to the Austrian alps – Oct 2015

As we cruised around southern Germany and then headed into the Austrian alps, we marveled at the M6’s amazing suspension and control. It inspired a sense of calm control as it hugged the turns, and the lack of strain on the engine was almost spooky as we cruised along at 120+ miles an hour on Autobahn straightaways. At one point, things got surreal as we were passed by a Porsche for poking along too slowly — at over 120mph!

While my hands gripped the steering wheel of a $120k+ piece of metal hurtling down the road at unreasonable speeds, I was amazed by my lack of nerves. On the one hand, the rational part of me was wondering just how much control I could possibly have at those speeds, but on the other, the high-tech braking and suspension system set my mind at ease.

My point in telling this story is that we all like the illusion of being in control, but the truth is that we never are completely in control. But if we focus on that and never get the car out of the parking lot, we’ll never get anywhere we want to go. Unfortunately, life is too short for that, from an investing standpoint. To meet your retirement goals, you have to be investing consistently, in both good and bad markets.

A much better approach is to decide ahead of time what your strategy is going to be, based both on where you want to go and who you are as a person. For example, if you know that the Autobahn fast lane is too much risk for you, maybe you would feel comfortable in the middle or slow lane. The problem is that people often go from parked to the fast lane and back again, all at the wrong times.

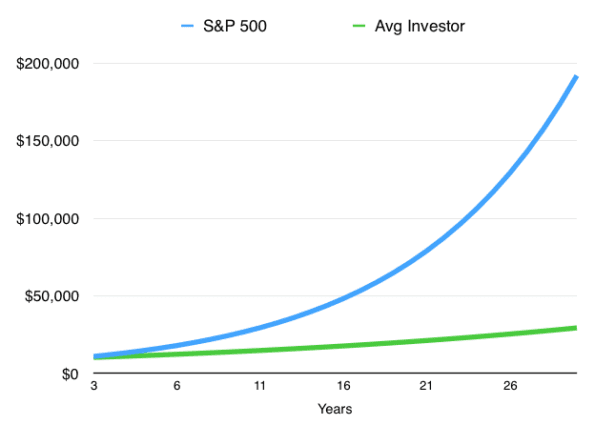

The market research firm Dalbar does an annual study of the average investor’s returns compared to the market indexes (loosely, an index tracks the average return of the market as a whole). The results are discouraging for the average investor — over the last 30 years, individual investors, on average, have underperformed the S&P 500 index by almost 7% per year. What does that mean in dollars? Let’s just say it’s not pretty…

This is what happens when you underperform by almost 7%/year over 30 years. The S&P 500 index (which represents roughly 80% of U.S. stocks, including the vast majority of large American corporations) has returned 10.35%/year over that period, while Dalbar reports the average investor has achieved a measly 3.66%/year return. This chart shows those returns on an initial investment of $10k over a 30-year period.

In its study, Dalbar was able pinpoint some of the most important reasons for this tragic underperformance. Coming in at number one in importance?

Analysis of the underperformance shows that investor behavior is the number one cause…

What this means is that the old investment axiom is true when it says, “it’s time in the market that matters, not timing the market.” What most investors tend to do when markets fall, is to sell investments to protect themselves from losses. If we step back for a moment, we can see that selling after a market downturn is the exact opposite of what we really should be doing. We want to buy low and sell high, right?

Other investors aren’t as prone to sell in a panic, because they are hardly ever invested at all. Trying to conserve capital, they only invest when conditions are “perfect,” which of course is exactly never. So, their portfolio limps along year after year, capturing just a fraction of the wealth produced by the best passive wealth-creator ever invented (e.g. stocks).

For these simple reasons, investor behavior is the biggest reason for underperformance. And to combat this, I recommend simply automating your investments. In my next post, I’ll explain several options for doing this. To some extent, there are better and worse options, but there is no “perfect” strategy. A lot depends on you and your circumstances, but the most important advice I can give is to find an automated solution that works for you, and then resist the urge to tinker with it. The only time you should change your strategy, in my opinion, is when you and/or your situation changes. It should not be based on the market.

Ready to get started? I’ll have a new post soon that explains how to automate your investments. Until then, sign up for the email list to make sure you don’t miss any new posts as they come out.

1This assumes the following: an investor with the median U.S. household income (currently about $50k/year), a saving rate 10%, an investment return of 11% on average (the average annual return of large and small US company stocks since 1926 is about 10-12%), and a 3% inflation rate. At age 65, this hypothetical investment portfolio can withdraw 4% (which most academic research has shown to be a safe withdrawal rate) and replace the inflation-adjusted pre-retirement income. Social Security retirement benefits are not included.

{kind=link}