Dave Ramsey is a popular personal finance educator who espouses a philosophy of avoiding debt at all costs. He points to all the negative consequences of abusing debt, with an overarching theme of how big, evil credit card companies and banks take advantage of the naivete of ordinary people, driving them into a lifetime of modern-day slavery to their credit card and other consumer debt. But what Dave won’t tell you is that there’s actually such a thing as “good debt.”

Right before I finished grad school and moved to Atlanta for my first real job as a financial planner, I sold my house. Now, this was before the housing bubble had burst, and thankfully I was able to sell it for a little profit. It definitely was not a huge amount of money, but it was a lot to me. I’ll never forget walking away from the bank after the closing and pinching myself because I had “so much money” in the account.

So, now I had a choice–I could pay off my student loans or invest the money. Since I believe in owning stocks as one of the best ways to build wealth, I chose to invest the full amount in stock mutual funds, rather than pay down debt. Almost immediately the market would test that decision as the Great Recession hit and stock prices were cut by about 50%. All that hard work I had put into that house–all the hours of fixing it up and making improvements–went seemingly down the drain in just a few months.

Almost immediately the market would test that decision as the Great Recession hit and stock prices were cut by about 50%. All that hard work I had put into that house–all the hours of fixing it up and making improvements–went seemingly down the drain in just a few months.

Or was it? As I continued to stay invested over time, the value of my investments inched back upwards. Now as I look back about a decade later, the market is up about 120% since before the crash, or about a 8%/year return. (Note, that return includes the market crash of 2008.) Since my student loans were at a lower interest rate than that, plus I got some tax incentives on the interest, I came out ahead in the end.

Dave Ramsey Was Both Right and Wrong

So, is Dave Ramsey wrong about avoiding debt at all costs? In my case, mathematically I was right, not Dave. My theory was that the long-term return of investing in stocks would earn more over time than paying off debt, which would only “earn” me the interest rate that I would otherwise have had to pay on that debt. When you compare those two options from that perspective, it seems obvious which one is right.

However, as I’ve gotten older (and hopefully a little wiser), I seen a lot of people run into problems with that kind of thinking. Sure, if the world worked like a spreadsheet, the answer is always to invest over paying down debt, as long as you can earn more on your investments than the interest rate on the debt.

However, life isn’t like a spreadsheet.

Still, contrary to Dave, I do think that there are some situations where it’s acceptable to use debt. The key is knowing how to use debt to improve your financial situation, without destroying it. However, the older I get the more I appreciate Dave Ramsey’s perspective on debt. As he often points out in quoting from the book of Proverbs, “the borrower is slave to the lender.” Misusing debt can lead to a never-ending pattern of living paycheck to paycheck. The abuse of credit is a financial epidemic in this country, and a tragic one at that. But that being said, I do believe that credit can be used properly, and with benefits both for the person borrowing the money and the lender as well.

But to really use credit properly, and carefully, we need to understand how it works.

An Overview of Credit

Like most things we invent, humans came up with credit to make life more convenient. In and of itself, it is neither good nor evil; it’s simply a tool that can be used wisely or unwisely. Thousands of years ago when humans were on the barter system, you had to exchange one good for another to get what you wanted. So, if you’re a wheat farmer, for example, and you want to trade some of your wheat to your neighbor for his latest barrel of wine, you might have a problem. While you want the wine today, your wheat harvest may not mature for months into the future.

What to do? Well, you simply ask your neighbor to give you some wine now, for a future amount of wheat at harvest time.

And so, credit was invented. That simple exchange was an early form of credit, because the wheat farmer is buying something today based on “income” he will have in the future. In other words, he is accelerating future income to the present to purchase something today.

Credit: The act of buying something today with income from your future.

Interestingly, many of the oldest writing samples in the word, in a script known as cuneiform from ancient Sumerian scribes, were everyday records of commerce. In fact, some historians argue that the Sumerians invented writing for the purpose of keeping track of their growing trade empire. They needed a way to complete mundane tasks such as tallying up grain receipts or drawing up a contract with a neighboring tribe. So credit may have been the catalyst for another important human invention — writing, but anyway, I digress…

The point is that credit is an important part of the modern day economy, because it allows for quicker and easier exchange of goods. And a faster-moving economy is a higher-producing economy, which means more jobs, more growth, and more tax receipts for the government….

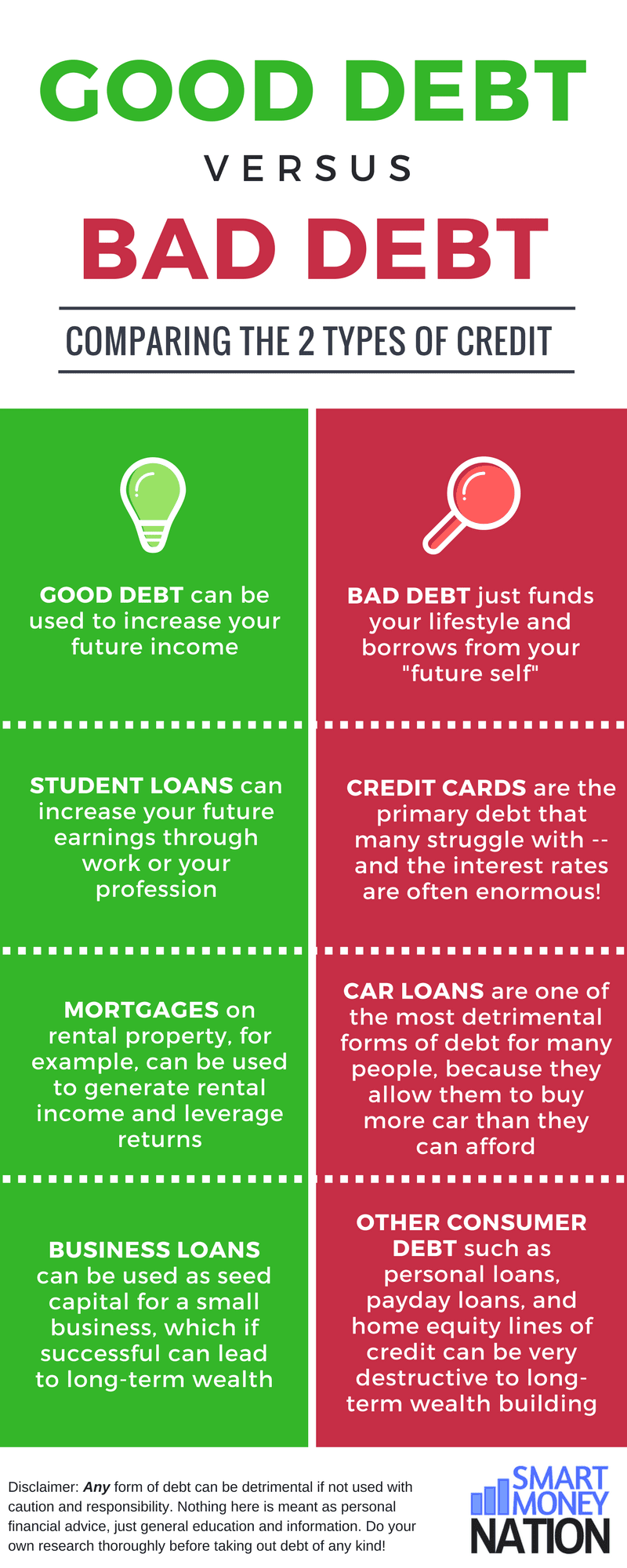

Good Debt vs. Bad Debt

But while credit, in moderation, is good for the overall economy, it can be very bad for your financial health if abused. And abusing credit is extremely easy to do, because money is constantly being thrown at us by credit card companies and banks.

The good news is there is a very easy way to determine if something is potentially “good” debt or “bad” debt. Remember that credit is borrowing from your future self to buy something today. So, it stands to reason that you don’t want to borrow money from your future self to buy something today that won’t increase your future self’s ability to pay off that debt when it comes due.

If that was confusing, let me explain. When you buy a latte using a credit card, for example, you’re borrowing from your future self’s income to buy that coffee today. You don’t have the cash to buy that coffee, so you charge it and go on your merry way. It’s future you’s problem, right?

The problem with this is not, in and of itself, the fact that you bought something on credit. The problem is that what you bought on credit doesn’t increase your future income.

So the more things you buy on credit today that you already can’t afford, you make life even harder for your future self to get ahead. Why? Three simple reasons:

- Future self also has to pay his/her everyday expenses

- And now the debt that you just created

- And on top of that the interest from the debt you just created

Future You is NOT going to be happy with Today’s You!

On the other hand, it IS possible to buy something on credit that increases your income in the future. That’s what I mean by GOOD DEBT. If you buy a real asset, one that will produce (or can be made to produce) income in the future, then you’ll have the money to pay back the debt plus the interest. The key is to buy something that pays enough additional income (or appreciates in value) to do that and still have more on top of that leftover.

For example, let’s assume you used good debt to buy a rental property. That rental property receives income every month, right? Therefore, you’ve increased your future income by buying that property, even though you didn’t have the full amount in cash today to buy it.

That is the fundamental difference between “good” debt and “bad” debt.

Examples of Good Debt

So, here are a few examples of what I consider potentially good debt. Now, you can probably find an exception to these broad categories. For example, while I list student loans as potentially a “good” debt, because in theory it increases your future income, a $200k degree in underwater basket-weaving probably doesn’t fit that mold. (No offense intended to the underwater basket-weaving community.) But generally-speaking, student loans can be good debt if they help you build skills to compete and earn a good income.

Could you get those same skills without going into debt? Maybe, and that would obviously be ideal. But I still think we can call student loans, in general, a better form of debt than, say, credit cards.

As a side note, you might find my post on the inspirational story of Dr. Wise Money interesting, because she was a master of finding creative ways to pay off debt. In her case, she could often make “bad” debt work like “good” debt. Read the post to find out more.

So here are some examples of Good Debt:

- Student Loans – you have to be careful, because, again, people take out huge loans for degrees that can’t help them get a good job. But in some cases these can be “good” debt.

- Mortgages on Rental Property – but be careful not to overextend yourself. Always keep enough equity to protect against a real estate market crash, as well as some cash reserves for repairs and vacancies.

- Business Loans – again, like any debt, these can be easily abused. But if the business is successful then, obviously, using debt is a lot quicker way to get started.

- Credit Cards – ONLY IF used strictly as a cash management system, and not to finance lifestyle purchases. In other words, if you pay off your credit card IN FULL every month, on time, you can rack up tons of rewards and also build your credit. The key is discipline and planning.

Examples of Bad Debt

Unfortunately, there are a lot more ways to misuse credit than to use it correctly. Here are a few of the many possible examples:

- Credit Cards – hopefully, I don’t need to say this, but buying things you can’t afford on credit cards can kill your financial future. The interest rates are huge (often over 20%) and paying just the minimum payment just prolongs the misery as long as possible.

- Payday Loans – all I can say is “ouch!”

- Car Loans – probably America’s #1 wealth-killer, in my opinion. The average car payment is about $500/month; just imagine how much wealth that would be if invested over 40+ years. We’re talking millions!

- Home Equity Lines of Credit — I have seen these used smartly. For example, to increase the value of a home by taking advantage of unique real estate opportunities. Unfortunately, most of the time people use them as a “piggy bank” to raid the hard-built equity out of their homes.

- Other Consumer Credit — buying any sort of depreciating asset, such as furniture or home electronics on credit is, frankly, just dumb. Unless its at zero percent interest. Then it’s still a bad idea, because you get used to buying whatever you want now without feeling the pain of saving for it, but it’s a “less bad idea” than otherwise.

Benefits of “Good” Debt

Some of the everyday benefits of using debt wisely include building a good credit score, getting perks and rewards such as airline miles and cash-back, and tax advantages (on mortgage interest, for example.) But the most powerful benefit of credit is the concept of “leverage.”

An in-depth discussion of leverage is beyond the scope of this post, but I’ll just say here that leverage is just what it sounds, it works like a “lever” to increase your investment return over what you could achieve with cash alone.

An example might help. To keep things simple, let’s assume that you buy a rental house for $100,000 and put up the customary 20% as a down payment. This particular property rents for $1000/month, and your total expenses including mortgage interest, maintenance and repairs, taxes and insurance, is $800/month. So you net $200/month from this property, which is a return of %12 on your original investment of $20,000.

Now let’s compare that to if you had not borrowed the 80% to buy the property, but instead you paid for the whole thing–the whole $100,000–in cash out of your own money. In this case, you do not have to pay the mortgage payment, and therefore can net much more from each rent payment. In this case, you can now get about $600 net each month in rent. Is that a better deal? Are you making more money?

Yes, you are making more in dollar terms, but actually less as a percentage of your initial investment. Believe it or not, your investment return has actually gone down. Why? Because the mortgage acts as a “lever” to increase your return. In this case, the unleveraged rate of return would be 7.2% ($600/month times 12, divided by your investment of $100,000.)

While Debt Can Increase Returns, it Also Increases Risk

Lest I give you an overly rosy picture about good debt, let me add one more clarifying detail. In the above example, I showed how the return on a rental property can be almost doubled by adding good debt. While that is true, and a well-known financial principle, it should be noted that leverage works both on the upside and the down. The Great Financial Crisis is a classic example of this. Many investment banks were leveraged 20:1 or even 30:1 on CMOs and other complex debt instruments. And when the economy turned, many of these banks went bankrupt or had to be “bailed out” by the Federal Reserve.

It works that way on a personal level too. Debt can be a powerful tool, both for good and for bad. If you decide to employ “good” debt, please use sparingly and cautiously.

So, what do you think? I’d love to hear your thoughts and perspectives below. Feel free to disagree as well… I promise not to be offended 🙂

{kind=link}

Nice looking website. Congrats on the startup.

Awesome article. As a Dave Ramsey follower (sort of), I agree with you that not all debt is dumb. Mortgages, student loans (if not too much), and credit cards if paid in full each month.

I have two reward earning credit cards and have them hooked up to Debitize, automatically pulling money from my checking account to cover my purchases.

Looking forward to seeing more of your great stuff.

Thanks Shin! Yes, that is exactly my strategy with regards to credit cards, except I haven’t checked into Debitize yet. Would love to hear how that’s working for you…? So far, the rewards cards have paid for several of my trips, and are paying for another trip coming up this summer. Cheers!

I think it depends. I don’t agree with Dave Ramsey’s don’t save for retirement. Only thousand in savings!!!

As for auto loans it depends. I bought a new car when my old car broke down. I looked at used but as female alone it was uncomfortable and I wanted a warranty I got a car with 100k warranty/10 year. Plan on driving it forever pay way less than $500.

I also bought a washer and dryer on installment my mom lives with me and the two of us would be $80 bucks a month to use laundry mat. The washer and dryer paid for itself in less than a year.

But yes lates and trips used for credit card how I regret. And my student loan was useless.

Now though I can pay washer dryer with my savings.

I am going to focus not on investing but paying student loans off with bonus at work. I do have my retirement savings. I would just not like to have that debt.

Great points, Becca. Thanks for visiting!