If you’ve spent much time reading financial blogs, you’ve probably run across the advice to invest in stocks for the long run. Among financial advisors, in fact, it is such a core belief (that stocks will outperform most other investments classes for the long term) that saying anything to the contrary is almost akin to blasphemy. This makes sense when you consider that over the last 90 years the stock market has had a positive return in nearly all rolling 10-year periods and have outperformed bonds nearly 90% of the time. In fact, over that time the stock market has averaged a very healthy 10-12%/year in total return, while bonds have posted an annual return of about half that amount. So history does back up this advice, and most people are happy to stop there and believe the issue settled.

But is it? To play the Devil’s advocate, aren’t financial advisors also the folks that are commonly saying that “past performance is not necessarily an indication of future results?” So how do we know that just because stocks have done well in the past they will continue to do so in the future?

To make matters worse, if you watch the financial pundits on CNBC or it’s equivalents, you will inevitably come across the “professional bears.” These are a group of analysts, economists, or asset managers who make their living selling pessimism, fear, and gloom. Their viewpoint is exactly the opposite–that everything is about to unravel, or at least, that future stock returns will come nowhere close to the levels of the past.

While all of this “noise” makes for great financial television, it is hardly helpful for your wallet. But what if I told you there are fundamental reasons why stocks tend to go up over time? Instead of just hoping that the past will look like the present, what if there were unique driving forces that propel them ever upward, albeit in a choppy fashion? (Check out the keys to successful long-term investing in volatile stock markets here.) Well, that’s exactly what I’m going to attempt to show you in this article.

Why Understanding This is Crucial to Long-Term Investing Success

But before we dive in, let’s take a step back and consider how this is crucial to your long-term investing success. Financial portfolios are largely defined by the basic breakdown between major asset classes. That is to say, the percentage of stocks versus non-stocks (bonds, cash, and other asset classes) in your portfolio will largely drive the risk and return characteristics of that portfolio. (The seminal study that showed this was published in 1986 in a paper called “The Determinants of Portfolio Performance,” published in the Financial Analysts Journal.) So it is far more important the overall breakdown you have between stocks and bonds than the percentage you have in Coke versus Pepsi, for example. (For more on this, check out why you should not waste your time picking stocks, and also the importance of staying diversified.)

Many investors have the misconception that investing stops when they reach retirement. Unfortunately, unless you just have gobs of money, you will probably have to continue to invest in retirement, albeit in probably a more conservative asset allocation strategy. This is because you need to earn returns high enough to replenish to at least partially replenish the funds you withdraw on an ongoing basis. According to the now famous Trinity study (or infamous, depending on your viewpoint),1 retirees can typically afford to withdraw about 4% on an annual basis and expect not to run out of money in old age. The reason it is so low is to account for ongoing inflation and for intermittent years of bad returns. That is why understanding the foundation of stock returns is so important. It allows the investor to avoid panicking when times get rough, and to keep faith in the strategy because they understand the foundations of returns.

The Building Blocks of Stock Returns

In an economy that is growing, each month businesses (in aggregate) are selling more goods and services than they did the month before. In this situation, business owners are incentivized to reinvest their profits back into the business. They can do this in several ways: they can hire more manpower, build more stores or factories, or invest in research and development to innovate cheaper and faster ways of doing things.

And why do any of these things rather than just pocket their earnings? Because they want to sell more goods and services (whatever that business sells) to make more money in the future. When they achieve that goal, it puts them back in the original situation of having more excess profits to reinvest back into their business again. It becomes a powerful loop of growth that every businessowner (or stockholder) wants to see.

Now when you own a stock, you are legally a part-owner in that business. Yes, technically you have a very, very small ownership stake in the entire business as a whole, but you are still legally an owner. So when the managers of your business reinvest your profits back into the business to generate even more profits, those profits are technically your money that you’ve reinvested back into the business.

So let’s talk about how those profits eventually turn into a return on your stock investment. The basic “building blocks” of your return on a stock will come from the following four components:

Inflation + Dividend Yield + Earnings Growth + Change in Investor Expectations = Stock Returns

For bonds, in contrast, the return you receive is simply the interest rate that it pays (assuming you hold the bond until it matures). This is one of the reasons stocks are considered riskier than bonds because the returns are dependent on more variables at play. Let’s take a look at each one in turn, and consider why we can expect returns in the future similar to what we have seen in the past.

Inflation

Inflation is simply a measurement of the change in prices across the economy over time. So if we say that inflation has been 2% over the last 12 months, we mean that the price of goods and services that we all buy to live have increased in price, on aggregate, by 2% over the last year. If you go all the way back to 1926, the general U.S. inflation rate has averaged about 3%/year. (See my recent article on why a little inflation is good for the economy for more on this.) Now, if everything is going up in price, and your investments don’t at least return the rate of inflation, then you are losing money in reality. That’s what we call your real rate of return, and it’s the first building block for stock returns because stocks are generally easily able to keep up with inflation. Why? Well, simply because companies can overcome rising costs by passing them on to their customers. So, the value of a stock itself should easily at least keep up with the rate of inflation.

Dividend Yield

The next building block of stock returns is the dividend yield. This fancy-sounding financial term is actually very simple: it means the profits that the company pays out to its shareholders (or, partial owners) at the end of each quarter. So let’s use a hypothetical coffee shop as an example (think Starbucks SBUX, for example). Let’s say they sell $1 million dollars worth of coffee in their most recent quarter. After the accounting is done, maybe 80% of that will go towards expenses (e.g. to pay the baristas for their hard work, buy the coffee imported from all over the world, keep the lights on, etc.)

That leave 20% as profits, or $200,000. Now, our little coffee shop company is publically owned (like Starbucks), which means it has investors on the stock exchanges and the everyday investor can buy the stock in their investment accounts. To keep it simple, we will assume that there are 100,000 shares outstanding for this company. So then, the easy math is that there will be $2 in profit for each share. However, the company wants to expand and build a new coffee shop next quarter, so it will need to use $100,000 of the profits to do this. That will leave $100,000 for the dividend payout to investors, or $1/share.

If we assume that the stock is currently trading in the market for $200/share, then the dividend yield is easy to calculate as follows: $1 dividend x 4 quarters = $4 dividend per year / $200 price = 2.0% dividend yield.

Nowadays companies generally pay less in dividends than they did in the past, for many reasons. However, they often do other things that have the same effect as a dividend, such as a share buyback program. Either way, dividends are an important part of the total return on investment for a stock.

Earnings Growth

Going back to the illustration of the coffee shop, we said that the company planned to use $100,000 from its profits to build a new coffee shop. Once completed, the company can now expect to sell twice as much coffee with two stores as it could with only one. And that means twice as much in profits for investors to receive, either in the form of dividends or in earnings growth.

So earnings growth is simply a measure of the increase in profits of a company over time. Historically, if we look at corporate earnings growth and compare it with general growth in the economy, we see a very strong correlation. Basically, as the economy grows, companies also grow their profits. (Of course, it doesn’t have to be this way, but the only way it would be otherwise is if the corporate sector shrank significantly relative to the economy as a whole. I find this to be very unlikely over very long stretches of time.)

So to put this in simple terms, if we can expect 3% economic growth in the U.S. (approximately the long-term average), it is reasonable to expect roughly the same amount of corporate earnings growth as well.

Investor Expectations

The last variable is the most fickle and difficult to predict because it depends on the perception of investors as a whole, and what they are willing to pay for a company’s earnings. You see, when an informed investor buys a stock, he or she is really buying a right to receive the future earnings of that company. So the price he pays for the stock is a reflection of how much he is willing to pay for those future earnings.

To use a simple example, let’s say I’m an apple farmer. Now I know from experience that one apple tree can produce so many apples, on average, per year. So from that, it is easy for me to figure out what I am willing to pay for one apple seed, based on the price per apple in the marketplace.

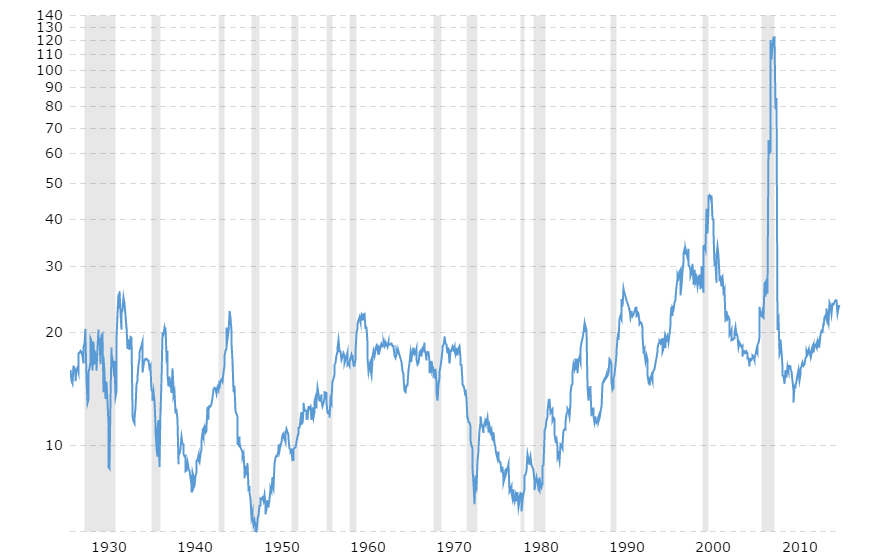

It’s the same way for stocks. Analysts have devised a simple formula to calculate what investors are willing to pay for $1 in corporate earnings called the Price-to-Earnings Ratio, or P/E ratio. As you can see from the following chart, investors have been willing to pay a little bit more in recent years than in the past. There are many reasons for this, but for our purposes, it’s important to realize that the higher the P/E ratio is, the more likely it will be lower in the future. If it just stays the same, it will no effect on the total return of a stock; however, if it goes down, it will hurt stock returns.

(And, obviously, if it goes up, it will help them.)

Yet recent P/E levels are not so high as to provoke extreme worry, in my opinion. Even if they merely stay at current levels, the stock market as a whole can achieve reasonably good returns, especially when compared to the historically low rates of interest offered in the bond market as a whole.

Why It’s Reasonable to Believe Stocks Will Continue to Provide Strong Long-Term Returns

Now that you understand the basic building blocks of stock returns, let’s put it all together using the formula above. Currently, inflation is running at about 2% in the U.S., and the dividend yield on the S&P 500 is about 2% as well. In addition, economic growth has been running roughly at about 2% since the Great Recession, and we have already said that we don’t expect a significant increase in investor expectations (as reflected in the P/E rate). Adding those up, we get an expected return of about 6% from stocks over the next 10-15 years. As a point of comparison, the 10-year Treasure bond in the U.S. is currently paying only about 2.4%.

To return the question of why stocks can be expected to go up over the long term, consider the four components that we discussed. Inflation should be expected to continue in the future, hopefully at a fairly moderate pace. (Remember, a slow and steady inflation rate is actually good for the economy.) Dividends (or stock buybacks) can be expected to continue as companies seek to reward investors for holding their stocks. Economic growth, while it has been slightly lower than average since 2009, has continued at a reasonable pace. Of course, a recessionary period would change this temporarily, but general economic growth can be expected to continue in the future as long as we have population growth and productivity growth (the two crucial components of economic growth).

Last, investor expectations go up and down in a cyclical manner over time. At extremely high valuations, such as the tech bubble of 2000-01, stock investors do well to be cautious. However, most of the time valuations are either neutral or positive to stock returns and even when they are higher than average, the timing of P/E compression is generally impossible to predict.

So to conclude, for all of the above reasons, I believe we can be confident that stocks will continue to provide strong returns, above that of most other asset classes, over the long term.

Notes:

1) There have been many criticisms of the Trinity study over the years, some of which I agree with. However, it is a handy starting point for a discussion on safe withdrawal rates in retirement. I list it here simply for reference and not as a recommendation.

{kind=link}

I love to visit your web-blog, the themes are nice..`”~”