Nowadays, if you work for a company that has a retirement program, it’s most likely going to be some variation of the 401(k). These plans have largely replaced pension plans as the vehicle of choice for companies to offer retirement benefits to their employees. And I’ve personally always been a pretty big fan of the 401(k). Sure, they aren’t perfect, and many financial bloggers and advisors out there prefer other options like IRAs and Roth IRAs, but I think the 401(k) still retains its place as one of the best ways most people should save for retirement.

I say this for several reasons:

- Higher Limits – Most retirement plans have contributions limits, which is to say there’s only so much money you can put into them. That’s because the government is giving tax breaks to those who participate, so they want to make sure the rich don’t take advantage of their generosity and use them as “tax shelters.” So, for example, the IRA and Roth IRA have limits of $5,500/year (and you can only choose one or the other, not both.) The 401(k) also has limits, but they are $18,000 ($24,000 for those 50+), and the company can still put in matching contributions above that amount. The bottom line is that most people will need to save more than $5,500/year for retirement.

- Pay Yourself First – The 401(k) allows you a quick and easy way to “pay yourself first” (or, save money out of your paycheck before you get a chance to spend any of it.) In fact, it is literally first, because you get a tax deduction on your contribution, meaning that you pay yourself before even the tax man gets his piece. That’s really first!

- Reminders – We all need to be reminded every once in awhile to save for retirement. With all the other needs and wants clamoring for your money, long-term goals can get swept under the rug. That’s why it’s helpful when your open enrollment comes around for work every year. It’s just another reminder to up your 401(k) contribution rate.

- Incentives – But the most important reason 401(k)s are a great way to save for retirement is the incentives that your work offers. Some plans offer a matching contribution to encourage you to contribute. Be sure to at least contribute enough to get the full match offered, otherwise you’re just giving away FREE MONEY!

And now, with the introduction of the Roth 401(k), you can add flexibility to that list, because now you can choose whether you want a tax deduction up front or in retirement. Not sure what I mean? Check out this post on how to choose between before-tax and after tax contributions.

Of course, the 401(k) does have it’s drawbacks, such as higher fees (often) and fewer investment choices (most of the time). Still, on balance I think it’s clearly the best way to start saving for retirement for most people.

By the way, I came across this great video from John Oliver’s Last Week Tonight that’s pretty dang funny, and actually gives some decent advice. Check it out:

How Much Should I Have in My 401k?

Nobody likes to talk about money, much less how much they have in their 401k. It’s one of those “off limit” topics, like sex and religion. But it’s important to occasionally take a hard look at where you are in relation to where you want to be, so that you can make the necessary adjustments, if needed.

When it comes to money, I always encourage people to look at where they are in relation to their own individual goals, as opposed to comparing themselves to others. However, for an article like this, I obviously can’t know each individual reader’s personal goals and aspirations. For example, if you’re passionate about retiring early and devoting your life to charity or an important hobby, then obviously you should be aggressively funding your 401(k) retirement account and therefore should have a much larger account balance at an earlier age.

On the other hand, if you’re perhaps self-employed, and devoting all your time and money into building your business, the 401(k) balance will likely be a smaller piece of the puzzle to look at. If your business succeeds, you may be able to retire and live off the income, with your 401(k) as gravy on the top.

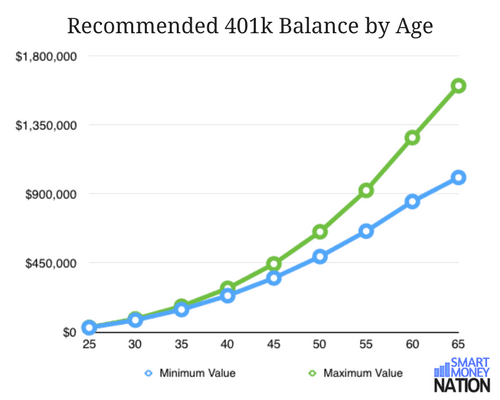

What Is the Right 401(k) Balance for My Age?

With all that said, I think it is still helpful to look at a hypothetical couple just saving for “normal” retirement goals (as if there is such a thing) to see what their 401(k) balance should be at different ages. Obviously, whenever you are running any sort of projection into the future, a number of assumptions have to be made. I will detail all of them at the end of the article, but the basic idea is this: I’m assuming the median family income in the U.S. for married households (median means half were lower, half were higher) based on the most recent census data.

In addition, I’ll assume that this hypothetical household starts saving 15% towards retirement as soon as they graduated college at age 22. Last, I’ll use a range of investment returns based on historical data but reduced slightly to be more conservative. (Again, see the assumptions at the end of this article for more details.)

Also, if you’re interested in what kinds of long-term returns you can expect to get from stocks, check out my recent post on that topic.

So, how are you doing? Are you within the values listed for your age? No?

Well then, that’s the reason for this post, to answer the question: how much should I contribute to my 401k?

How Much to Contribute to 401k in 30s

So we’ve already established that if you start early enough, you can probably get away with only a 10-15% contribution rate to your 401(k). But if not, you will obviously need to increase that. By the time you reach your 30s, you’re probably settled into a career and hopefully finished paying off those pesky student loans. So you can afford to put away a little more to catch up.

If that’s you, I recommend dialing up your contributions to at least 20%. You may find that is a little difficult, so here’s three suggestions to help:

- Give the Taxman a Hard Shove Outta the Way — Make all your contributions on a “pre-tax” basis, which means you get a tax deduction right away. Your payroll folks will withhold less for Federal and state income taxes, effectively easing the pain a little bit. Instead of losing 20% of your income, it will probably be more like about 13-15% after the reduction in taxes.

- Focus on Yourself First — If you have kids, this next recommendation can be hard, but I sincerely think it’s 100% necessary. You have to save for retirement before you even think about college funding. Yes, paying for college is hard, but if push comes to shove, you (or your kids) can always borrow money for college. Or, perhaps they can work and go to school at the same time. Or, they could even try the smartest way to pay for college. I don’t have space to detail all the reasons why, so check out my post on why parents should save for retirement first before worrying about saving for college for their kids.

- Try the Anti-Budget — I like to do the right things the easy way. Basically, I trick myself into doing what I should do by “paying myself first,” and then seeing how much it hurts at the end of the month. So, I increased my 401k contributions gradually over time, until I could max them out without running into credit card debt or spending through my “emergency fund.” Here’s more on the anti-budget approach.

How Much to Contribute to 401k in 40s

Again, if you find yourself solidly within the numbers on that chart above, and aren’t trying to live like a baller in retirement, you can probably stick to the 10-15% contribution rate. Everybody else, it’s time to put our big boy and big girl pants on, and get to work.

Think at least 30% of your gross income.

I know that’s a painful number, but it is what it is. I can’t re-invent math for you, and to put in less but still get to a decent retirement is going to require unrealistic investment returns. To get them, you’re probably going to end up taking investment risks that you shouldn’t, just to try and catch up, which is a recipe for disaster in my experience. Don’t put yourself in that position. Check out You Need a Budget, get control of your money, and save, save, save!

How Much to Contribute to 401k in 50s and 60s

At this stage, what’s more important is the investment return (or avoiding permanent loss of capital) that is compounding your nest egg. Think of it like this, you can max out your 401(k) at the current limit of $24,000/year, but if you have a $1 million portfolio that gets just 5% in return, that’s $50,000, or double the amount of your contribution.

For this reason, an investment plan is absolutely vital for your financial health at this stage. Read about why you need to put your investments on auto-pilot here.

Still, if you are behind, it’s obvious that you should contribute as much as you possibly can. Once you’ve hit the max on the 401k, you can also use Roth IRAs (if eligible) or just a plain old investment account. Check out Betterment for a good place to start. Or Vanguard if you are more of a DIY investor.

Assumptions:

- Inflation rate: I used 3% which is the long-term historical average in the U.S.

- Returns: I used a range of 6-8% for the minimum and maximum values. This represents the average annual historical return for a balanced to moderately aggressive stock and bond portfolio since 1926. See my article on the long term return of stocks for more details. I have reduced those returns by about 1-2% further to be conservative.

- Income: Based on the 2015 U.S. census data, the median household income for a married couple is about $85,000/year. However, I’ve made assumptions about the income growth of our hypothetical couple in an attempt to be realistic about a “typical” career path. So they started with $40,000/year and their income grew to about $110,000 by age 65 (again, in today’s dollars).

- Today’s dollars: I’ve discounted all the values shown by 3% inflation to show the amount in “today’s dollars.” This article from Investopedia is helpful in explaining Time Value of Money and why it’s important.

- Retirement Income: I assumed the median income in retirement of $85,000/year, less the pre-retirement savings rate and FICA tax.

- Social Security: I assumed a moderate level of Social Security income, but altered to show a lower inflation rate on benefits due to the unfunded nature of the program.

{kind=link}